The Sound of Childhood

Why the next frontier in kids’ entertainment may be a speaker.

Hi there! I’m Maxime, and you’re reading Recreations, a newsletter about the intersection of media, technology, and culture.

You’re receiving this either because you subscribed or because someone forwarded it to you. If you’re in the latter camp, you can subscribe here or via the button below.

At bedtime, a child reaches for a padded cube. The room goes quiet. A story begins.

There is no screen to unlock, no feed to refresh, no algorithmic rabbit hole waiting. The interaction is deliberately simple. It’s a device that feels like play.

That scene captures one of the more interesting shifts in children’s media today. After years in which childhood entertainment was pulled toward smaller screens, faster formats, and more compulsive platforms, a group of companies is moving in the opposite direction. Over the past decade, players like tonies, Lunii, Yoto, Merlin, Joyeuse, and Eddi have turned children’s listening into a market of its own. Part toys, part media platforms, and part parenting aids, their products borrow the warmth of analog childhood and rebuild it for a generation raised inside digital ecosystems.

The timing is not accidental. Modern parents have grown anxious about attention, overstimulation, and the invisible mechanics of mainstream platforms. This makes them increasingly willing to pay for products that feel educational, developmentally sound, and aligned with family rituals. At the same time, a set of economic catalysts have given the industry both the content supply and the market opening it needed.

But the business is more complicated than its charming hardware may suggest. Scaling means confronting a series of trade-offs. Licensed IP accelerates adoption, but taxes margins. Original characters improve the economics, but take years to earn trust. Subscriptions can smooth seasonality, but require a deep and constantly refreshed catalog. Openness can expand the catalog, but may weaken curation. Interactivity can extend relevance, but risks drifting toward the engagement mechanics these products were designed to avoid. And as children grow older, every player eventually has to compete with video and gaming.

While many of these dynamics may feel familiar, the category’s real opportunity lies in taking audio seriously as a medium of its own.

This piece looks at the business of kids’ audio hardware: how the market is structured, why it’s gaining momentum now, and the forces and challenges that will shape its next phase.

Mapping the kids’ audio landscape

At first glance, the kids’ audio category may look like a single, uniform whole. In reality, it’s a stack of strategic choices across distinct but interconnected axes spanning age, form factor, catalog strategy, and more. Mapping those dimensions upfront will make it easier to understand what the next competitive battlegrounds may be for the space.

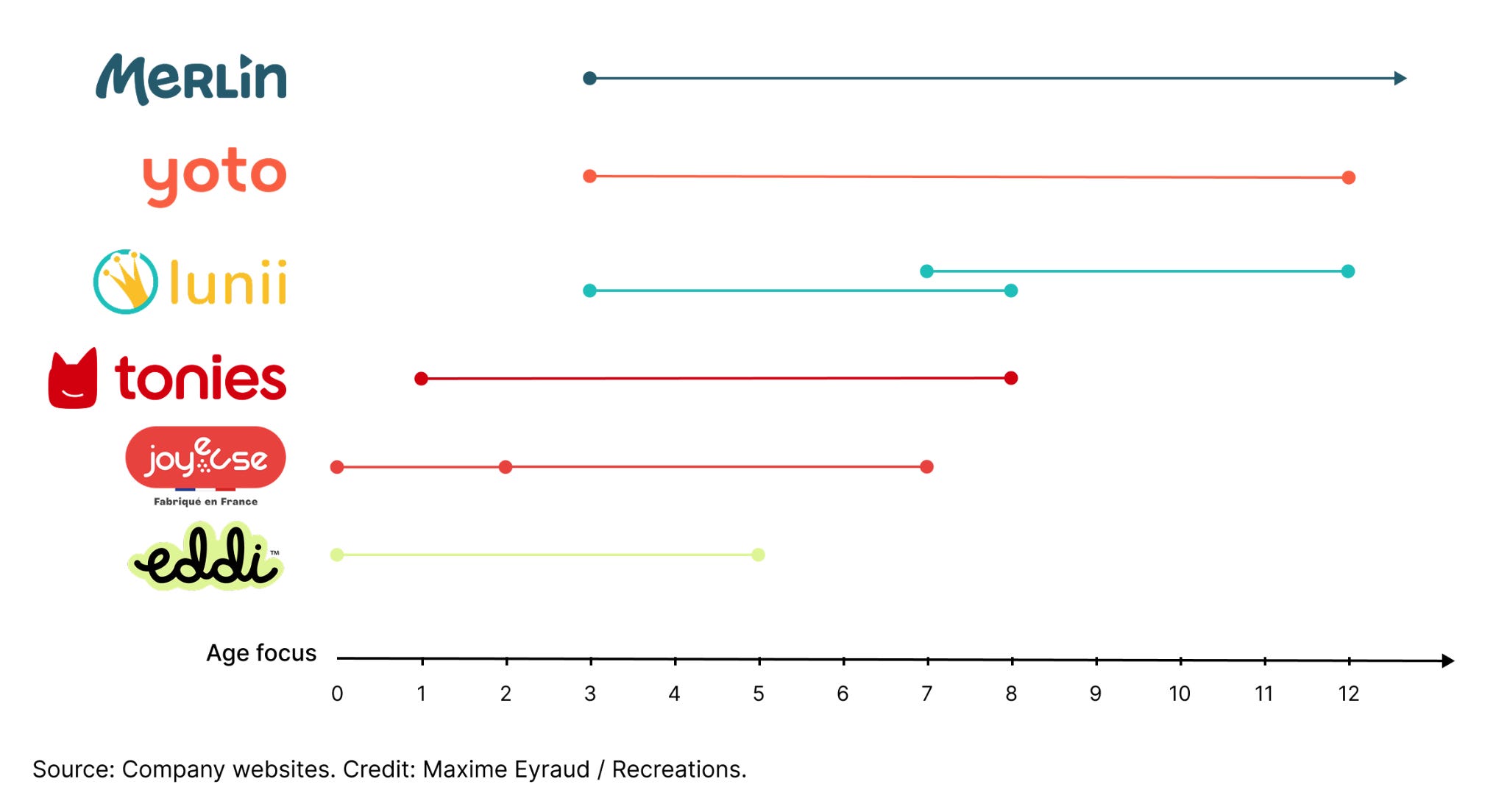

Age focus

A first way to segment the kids’ audio market is by developmental stage.

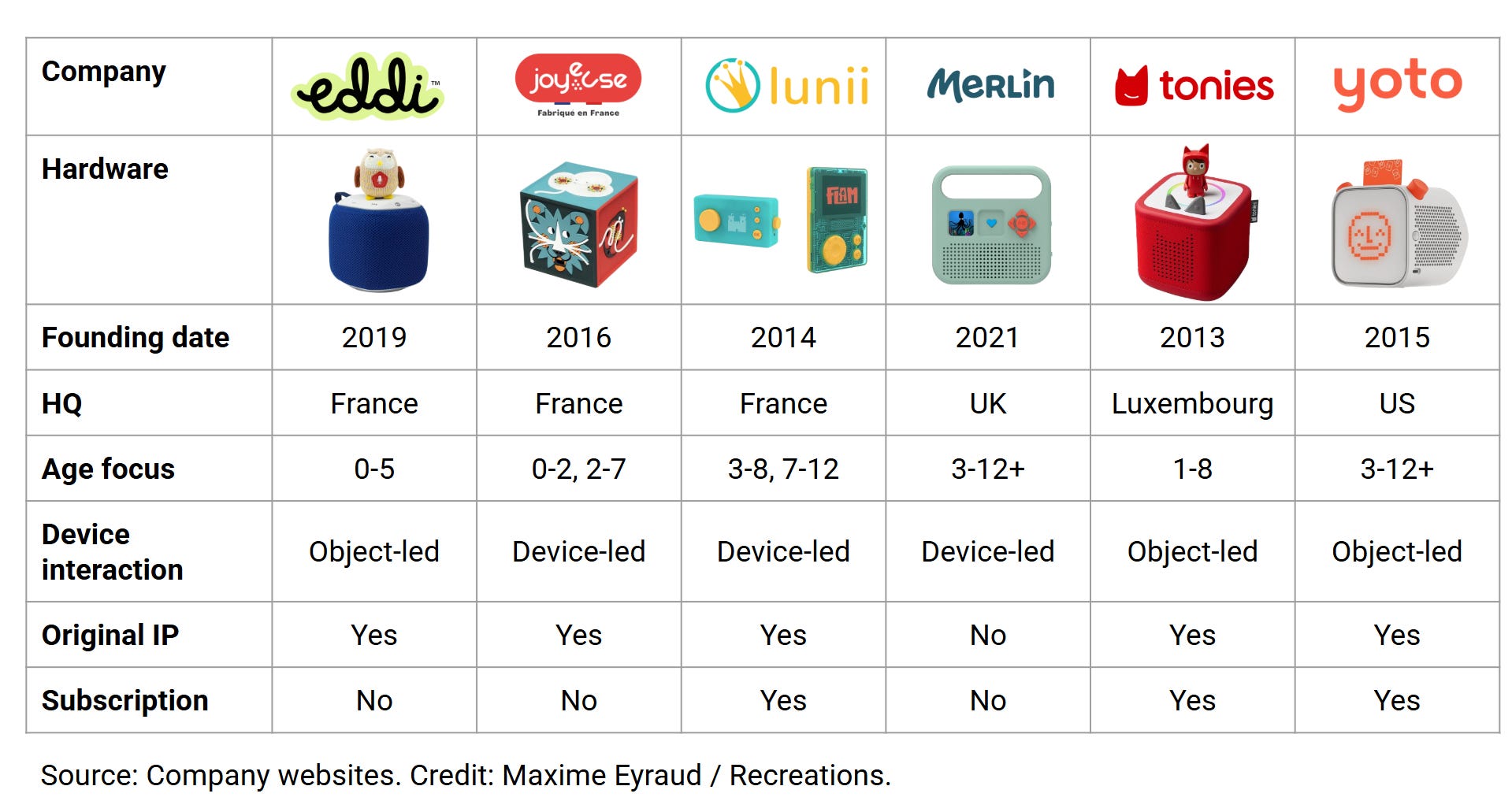

At the youngest end, the device functions mainly as a reassuring, highly mediated object tied to early routines. Joyeuse, for instance, has positioned itself almost from infancy onward, even describing Ma Première Conteuse as “the all-in-one toy for a child’s first 1,000 days”. At that stage, simplicity and parental control matter more than breadth of choice.

For preschoolers and early readers, the emphasis shifts toward independent use. This is where tactile interfaces such as figurines, cards, knobs, or large buttons become effective, allowing children to access content on their own without relying on literacy or abstract menus. This remains the category’s core segment.

For older children, the challenge becomes retention. As tastes broaden, expectations around content rise, and video’s pull becomes harder to ignore, some companies extend their catalogs toward podcasts and documentaries, while others introduce more advanced devices altogether, as Lunii did with FLAM, its player for 7- to 12-year-olds. For this age bracket, hardware can also sustain more elaborate interaction mechanics, with greater room for choice, progression, and active engagement.

Beyond just UX, age defines the length of the customer relationship. The narrower the developmental fit, the more intuitive the product may be, but the shorter its window of relevance is likely to be.

Device interaction logic

Another useful way to segment the category is by how children are expected to operate the device.

The first model is device-led: here, children navigate through buttons, dials, or other built-in controls to start, skip, replay, or switch content. That’s the approach Lunii, Merlin, and others have opted for. The main advantage is simplicity: the same device can support a broad range of listening uses without tying each piece of content to a separate physical object that could get damaged or lost. At the same time, it also makes the interaction feel slightly more abstract, especially for pre-literate children.

The second model is object-led: playback is triggered through a figurine, card, or similar physical item. This makes content selection concrete and easier to grasp and facilitates independent use, while turning content into something displayable, collectible, and giftable. Cuddle Tonies and Eddi’s Crafties — larger-size, “huggable” plush toys — are obvious examples here.

A related question is how much visual feedback the device introduces without becoming a screen-based product. Although these devices broadly position themselves as alternatives to video-based entertainment, some still incorporate limited visual elements. The Yoto Player features a low-resolution pixel display, while Lunii’s “My Fabulous Storyteller” uses light-based cues. Absent physical activators, the parent’s phone often becomes the hidden control layer in order to upload content, manage subscriptions, and oversee specific modes.

Catalog strategy

A third dimension has to do with how content is selected, packaged, and controlled.

On that front, players first need to offer a minimum viable catalog — enough size and breadth to reassure parents that the device will not be exhausted too quickly. At the time of writing, Lunii and Joyeuse each list more than 300 titles; tonies’ French store offers 241 Tonies figurines, each tied to a discrete piece of content.

Once that threshold is met, differentiation shifts from quantity to editorial identity. In some ecosystems, the catalog is built around familiar kids’ franchises that help drive brand recognition and purchase: tonies, for instance, routinely features some of its largest brand partners including Disney and Hasbro through what it calls “cross-franchise” marketing campaigns. Others, like Lunii, rely more on original stories, educational formats, or a broader editorial promise.

Either way, the real value lies in the curation: parents trust the company behind the speaker to assemble an age-appropriate universe, while children browse within a bounded set of safe options.

Ecosystem openness

Catalog strategy has an obvious corollary: how willing each player is to let families move beyond it.

In practice, this is not a binary “open or closed” divide. Most products now allow some form of uploading or recording, from Joyeuse’s Moulinette to Creative Tonies.

The more revealing question is not whether openness exists, but how central it is in the experience. For some players, it remains an auxiliary feature, useful for grandparents’ messages or a few personal files but clearly secondary to the proprietary catalog. The product still behaves primarily like a curated media environment, with the company deciding what belongs inside the child’s listening universe. For others like Yoto or Merlin, however, openness points toward a broader platform strategy, where the device can integrate content from multiple sources — publisher catalogs, podcasts, and even indie creators.

That distinction changes the boundaries of the product and business. A tightly curated ecosystem maximizes trust and editorial control. A more open one increases use cases and long-term relevance, but raises new questions around moderation, quality, and consistency.

Monetization

The final segmentation lens is monetization. Most kids’ audio businesses are built on a simple split between hardware and content. It’s worth unpacking their respective characteristics, and how they overlap to form a cohesive ecosystem.

Hardware is the entry point. The speaker is usually a one-off, or at least infrequent, purchase whose main job is household penetration. In practice, this emphasis means hardware is often deliberately priced and promoted in ways that prioritize adoption over short-term margin. Lunii, Joyeuse, and others all offer a 10% discount on the purchase of their signature speakers in exchange for subscribing to their newsletters — a sign that they value long-term customer engagement and ecosystem growth over a one-time revenue boost.

Content presents a far more attractive profile. Once produced or licensed, it can be reused, translated, and repackaged across markets far more efficiently than new hardware can be manufactured. Content also lends itself naturally to recurring revenue models like subscriptions, which help smooth out revenue over time and increase predictability. However, a subscription model requires sufficiently deep and continuously refreshed content libraries, something only established players such as Yoto, Lunii, and tonies have been able to implement so far.

The differences between the two segments are clearly reflected in the numbers. According to tonies’s FY2025 earnings presentation, Tonies figurines — which, despite technically being physical products, represent the content side of the business — generated 71% of total group revenue, versus 26% for Tonieboxes (hardware), and 3% for Accessories & Digital. The split still fluctuates, especially around holidays and major launches, but the direction is clear. Overall, content has been accounting for an increasingly larger share of total revenue over time: from 62% in FY2022, to 63% in FY2023, to 68% in FY2024, to now 71% in FY2025.

Still, things are not as binary as they may seem. For one, hardware still leaves room for higher-margin products. More than the speakers themselves, accessories including themed cases, backpacks, and headphones allow companies to extend monetization deeper into the household through purchases that sit closer to lifestyle and gifting than to core hardware. This improves revenue per installed device without materially increasing supply chain complexity.

Meanwhile, despite its scalability, content isn’t necessarily as profitable as it may appear. Similar to major platforms like Netflix or Spotify, kids’ audio companies will often forgo a substantial chunk of revenue in order to lure consumers in. At the time of writing, Lunii’s subscription offering, Lunii+, is offered at a discount, putting it at €6.90 a month for 3 months versus its usual price of €9.90 a month. Offers like these may accelerate adoption, but they only make economic sense if long-term retention can offset the lower ARPU upfront.

For the category, monetization depends less on the first sale than on what happens after the device enters the household. The strongest players are those that can turn hardware adoption into ongoing content consumption, repeat purchases, and broader ecosystem spend.

Taken together, these axes show that kids’ audio hardware is really a competition between ecosystem choices, not just devices. Those choices also reinforce one another: for example, a product like Joyeuse, built for very young children, can rely on simpler hardware mechanics and a narrower catalog.

Catalysts

These dimensions help explain how the category is structured. They do not, by themselves, explain why it’s gaining momentum now. To understand that, we need to unpack the cultural anxieties and economic conditions that make its proposition unusually timely.

Cultural catalysts

Screen fatigue and digital guilt

After more than a decade of screen ubiquity, parents are growing increasingly uneasy about the role digital devices now play in their children’s daily lives. Screen time has become one of the defining anxieties of modern parenting, linked to concerns over attention, self-image, and emotional regulation.

In that sense, kids’ audio hardware benefits from a first cultural tailwind, simply by offering a media experience that does not depend on a screen at all. For parents, that makes it feel less entangled with concerns over overstimulation and dependency. There are more practical considerations, too. With their rounded corners and soft materials, today’s audio devices are built to be handled, carried around, and dropped. That puts them in stark contrast with screen-based devices, which are often too fragile or too expensive to be handed over without supervision. In turn, kids’ speakers feel like a lower-stakes, more acceptable presence to bring into the home.

The unease is not just about the hardware, however. Within that broader digital anxiety, video raises a more specific set of concerns. On platforms like YouTube, the medium combines visual saturation with highly effective engagement mechanics — whether in the content itself, through bright colors and rapid cuts, or in the interface, through thumbnails, feeds, and autoplay. By contrast, audio asks children to build the scene themselves, largely avoiding the visual saturation and retention mechanics that shape so much of video consumption. For parents, that makes it easier to see it as a medium that preserves, rather than crowds out, their children’s creative autonomy.

Taken together, these qualities make kids’ audio feel like a more mindful and guilt-free form of technology — modern enough to entertain, yet insulated from more compulsive media patterns.

Enhanced parenting

As distrust of digital media grows, the bar for children’s products rises. If a child is going to spend time with technology, parents increasingly want that time to feel developmental rather than just entertaining. In that process, technology becomes a parenting tool.

The industry at large has embraced that language. Lunii says it offers “interactive audio experiences to support parents in educating their children” and is “establishing itself as a major reference in educational entertainment for future generations.” Eddi (formerly known as Storypod) describes itself as “an immersive Learn-and-Grow Audio System.” Meanwhile, tonies provides “a screen-free learning tool that focuses attention, enables creativity, and supports early learning.” Several players back their claims with hard numbers: a 2024 study conducted by the University of Wisconsin found that tonies users scored 32% higher than children who did not on their emergent literacy scores.

But these products do more than promise developmental benefits. They also let parents signal something about themselves. Buying a Toniebox, Lunii, or Eddi is a way of performing a particular ideal of contemporary parenting, one that’s intentional and curated. In that view, kids’ speakers become a marker of parental self-image.

Nostalgia for analog childhoods

Many of today’s parents are millennials who grew up with cassettes, CDs, and radios — specialized hardware that imposed a slower, more linear, and arguably more intentional relation to sound. Today’s kids’ audio hardware companies understand this perfectly. With their knobs and wheels, their products aren’t just appealing to children’s tastes but also echoing the physical vocabulary of 80s-90s audio devices that their parents grew up loving.

Some companies lean more heavily on this aspect than others. Yoto’s cards, for instance, directly mimic the insert-and-play experience of tapes or CDs. Similarly, tonies’s RFID-powered figurines, placed on top of the Toniebox, lean into the sort of physical interaction that’s reminiscent of loading media into a device. These design affordances do two jobs at once: they make the product easier for children to understand and easier for parents to trust.

Desire for rituals

The larger opportunity, however, is not entertainment alone. More and more, companies are trying to capture a larger share of children’s time by embedding themselves into rituals central to early development and to family life at large. Addressing such moments ensures repeat usage and anchors these platforms in emotionally charged, high-trust contexts where convenience and reassurance are key.

Nowhere is this strategy more apparent than around bedtime. As a ritual, bedtime is one of the day’s most codified moments, one that brings together routine, sensory calm, and emotional regulation, all under parental supervision. Audio content fits naturally into that window, receding into the background as a companion rather than a point of focus.

Companies have now leaned heavily into this use case, designing products that physically and behaviorally align with the ritual itself. Every player offers a variety of sleep-focused content, from bedtime stories to so-called “sleep sounds” or Yoto’s “sleep radio.” Both Lunii and tonies, for example, have developed bedtime-specific variants around their own proprietary IP, embedding them more deeply into everyday family life. The hardware actively supports these efforts. The Yoto Player includes a sleep timer and volume play limits “for night time curfews,” and turns into a nightlight when flipped down, with brightness controlled via a physical knob and colors by parents through the app. The second generation of tonies’s Toniebox offers similar features.

The point is not to maximize time spent — at bedtime, success means disappearing into the routine. The more tightly their devices can fold into these everyday rituals, the less they need to compete for attention at all.

Economic catalysts

Cultural demands help explain why parents have proven so receptive to kids’ audio. But the category’s growth also depends on a set of economic conditions that gave specialized players both the content supply and the market opening they needed.

Maturity of audio ecosystems

The rise of podcasts, audiobooks, and voice technology has normalized listening as a primary mode of media consumption and engagement. In the U.S., Edison Research estimates that audiobook listening among people aged 12+ rose from 21% in 2015 to 36% in 2025, while weekly podcast consumption reached 40%. Weekly podcast time has grown even faster, from 170 million hours in 2015 to 773 million in 2025, a 355% increase over the period.

With the audio habit now deeply ingrained, child-appropriate formats were a natural extension. In 2023, UTA found that around 48% of U.S. children consumed podcasts weekly. This opened the door for a myriad of kids-focused studios that are now producing a diverse range of content to feed that demand. Kids’ audio hardware is the child-facing expression of a much broader media habit.

Licensing and IP integration

The space is also riding a broader industry shift whereby IP owners increasingly treat audio as a must-have rather than a side format. In recent years, prominent rightsholders including Marvel and Ubisoft have extended their worlds through a mix of IP-centric educational podcasts and scripted audio series. Audio is now part of the standard transmedia toolkit, a way to keep worlds alive between larger releases and to multiply points of contact with audiences.

Kids’ rightsholders understand that logic too. For properties like Disney Princess, Paw Patrol, or Peppa Pig, audio storytellers are a way to cultivate and monetize beloved properties without the heavy lift of animation or film production and in a medium that parents already trust. This opportunity is especially relevant in France, where an unusually rich catalog of children’s classics — from Le Petit Prince to Babar and Yakari — remains largely underexploited outside books and traditional audiovisual adaptations. Lunii and Merlin are making the most of this dormant stock.

At the same time, a new generation of IP is entering the market. After dominating video, YouTube-native companies like CoComelon and France’s Animaj have been actively expanding into audio with fully-fledged soundtracks. At the time of writing, Animaj’s Spanish-speaking property Pocoyo has 1.2 million monthly listeners on Spotify; CoComelon has more than 3 million. As they continue to both acquire established properties — Animaj acquired France’s iconic Maya L’abeille in October 2025 — and launch new ones, the kids’ speaker category will be a logical outlet.

Premiumization of kids’ tech

Another tailwind comes from the gradual premiumization of the broader kids’ category. As parents have grown more skeptical of the average piece of digital entertainment — with its low-quality content and often aggressive monetization — they have become more willing to pay for products they perceive as developmentally sound and more aligned with their values. Today, that willingness is reflected across both physical and digital offerings, from premium developmental play kits like Lovevery to craft subscriptions like KiwiCo and all-in-one digital services like BayaM.

That trend changes the price logic of the entire category. Given the upfront cost of the hardware and the recurring spend on content, products like the Toniebox and Yoto Player compete less with low-cost toys than with high-consideration gifts. Their premium look-and-feel, educational claims, and the promise of repeated use enable them to command relatively high prices and reinforce their giftability.

Premiumization also makes the ecosystem economics more palatable. Parents may resist endless low-value digital upsells, but they are more open-minded when additional purchases are framed as additive to a durable and high-quality product. Premium positioning helps legitimize the ongoing sale of content, accessories, and subscriptions, supporting stronger lifetime value.

Platform gaps left by big tech

For all their scale and sophistication, big platforms have largely failed to crack child-safe UX. Some of the largest kids-focused products still inherit adult logics, whether in content, interface, or monetization. When safety controls do exist, they are often layered on top of discovery systems designed for adults, leaving parents to manage settings rather than trust the product by default.

That gap created fertile ground early on for independent players to emerge with radically different propositions. Hopster and Kidoodle, among others, emphasized editorial control and age-appropriate navigation and blurred the lines between entertainment and education. With limited but premium libraries, they traded needless abundance for clarity and control.

A similar dynamic has played out in audio, a medium the major platforms had long treated as secondary. Spotify Kids debuted only in 2020. As for hardware, while Amazon’s Echo Dot Kids came out as early as 2018, it remains a voice-first device, making it unfit for younger or pre-literate children.

The specific affordances of children’s audio — imagination, autonomy, ritual — remained largely underexplored as a result. This opened the door for specialized players to rethink audio from first principles and treat it not as a smaller version of adult streaming, but as a standalone medium. Lunii, tonies, and Yoto launched in 2015, 2016, and 2017 respectively and had years before large players made any serious push into child-centric audio hardware or UX. By the time Amazon or Spotify’s broader kids initiatives gained traction, the mental model for safe kids audio had already been shaped by these independents and their purpose-built systems.

Growth vectors

The category’s momentum is clear, but the next question is where growth can actually come from. For companies in the space, expansion is less about selling more speakers than extending the role these devices can play across content, use cases, and channels.

IP development and management

The IP conundrum

In kids’ audio, IP is both the growth engine and the margin tax.

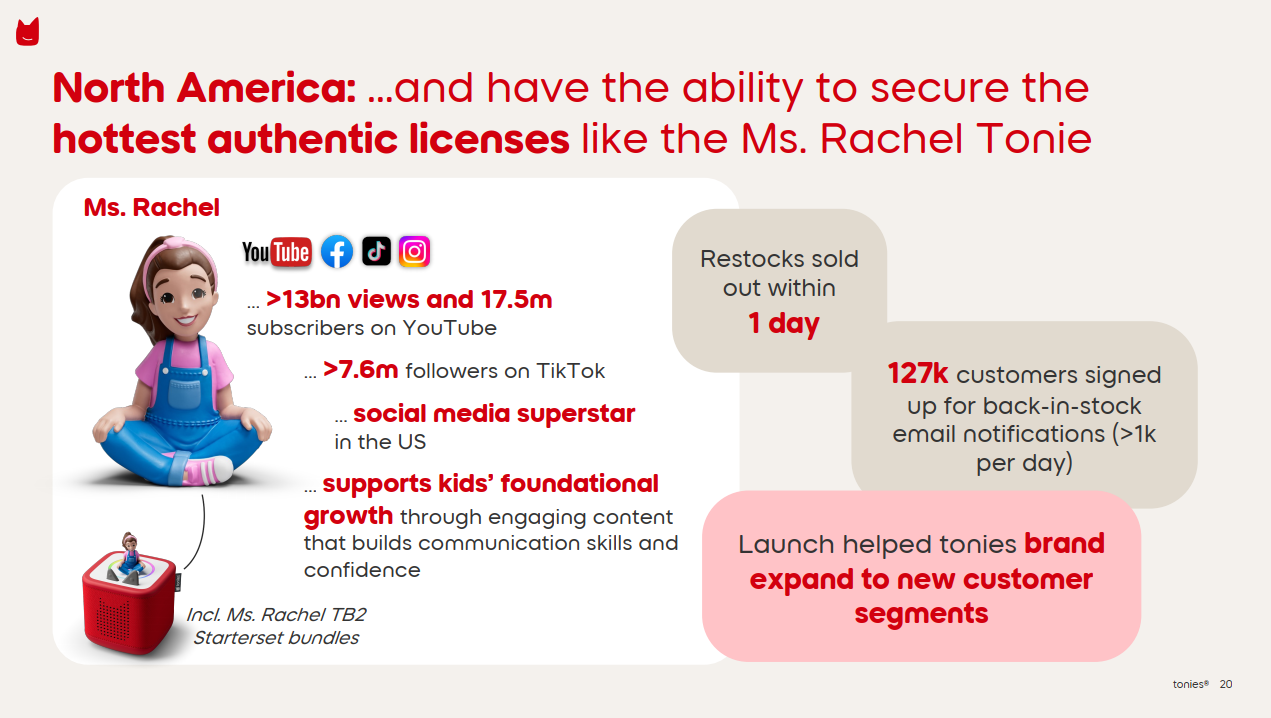

The upside is twofold. First, premium IP facilitates consumer adoption: for a busy parent standing in a toy aisle or scrolling a marketplace, recognizable characters are a shortcut for trust and quality. That makes licensed franchises a powerful acquisition tool, especially when the hardware itself is still a new behavior to adopt. tonies underscored this in its Q3 2025 earnings presentation by highlighting the Ms. Rachel deal and its pull on consumers. Second, IP unlocks distribution. Familiar franchises make a product easier to list and promote, giving retailers a ready-made hook and increasing the odds of prominent placements.

But the same mechanism also comes with downsides. First, top IP comes with punishing economics, as royalties scale with success. Unlike other levers that may benefit from economies of scale, licensing costs remain structurally tied to revenue. In practice, IP can become a material tax on gross margin — tonies’ investor reports show that its licensing costs have varied from 18.7% in FY 21 to 10% in FY 23 to 12% in Q3 2025, driven by product mix, renegotiations, and a growing share of in-house content.

Second, IP rarely stays differentiated for long. Indeed, IP owners have a vested interest in making their properties as ubiquitous as possible. The more licenses they grant, the larger their surface area and the higher the revenue potential. Given these incentives, exclusivity is hard to secure for long. That’s why the same top properties routinely appear across competing ecosystems. Premium IP may be necessary to play, but it’s rarely sufficient to win. Nor is the answer simply to add more content indiscriminately.

The limits of diversification

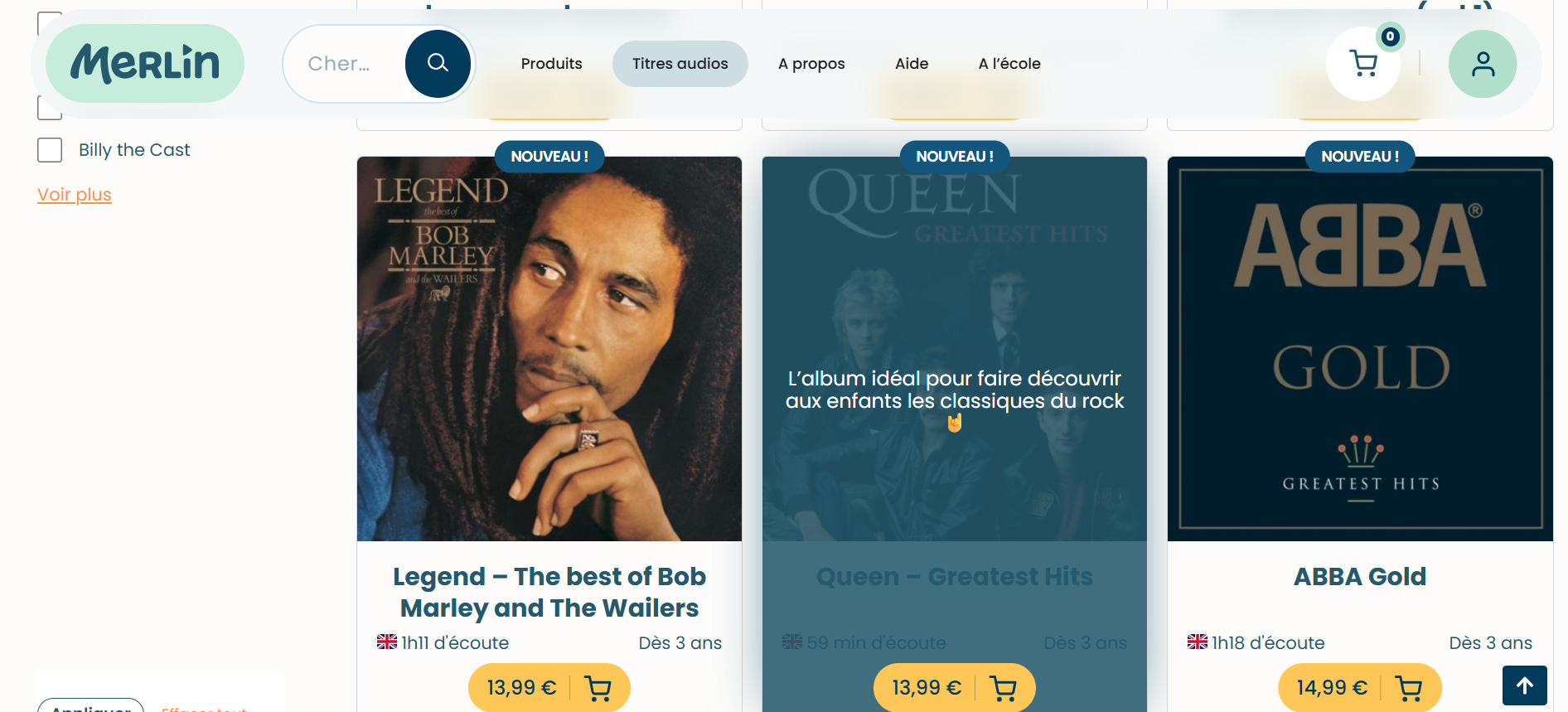

One possible response is to broaden the catalog beyond pure children’s storytelling and entertainment, into adjacent use cases like family rituals, music, or education — a form of diversification that increases engagement, embeds them deeper into household life, and strengthens their overall utility in the eyes of parents. Merlin offers a useful boundary case here: it shows both how far these ecosystems can stretch, and where that stretch starts to break down.

On the company’s store, parents can now find not only obviously kids-focused audio content, but also music from mainstream artists including Bob Marley, Queen, and ABBA.

On paper, the rationale is clear. Like nursery rhymes, mainstream music can help foster intergenerational listening moments — especially for older children, who are transitioning away from kids-only content and starting to more deliberately take inspiration from their parents’ tastes. The description for the Queen album, for example, presents it as “the ideal album to introduce kids to these rock classics.”

The problem is not editorial; it’s economic. Price is the main challenge: each of the aforementioned albums sells for roughly €14. While that may not seem excessive in isolation, it almost inevitably comes on top of a household’s existing subscription to a music streaming service like Spotify, which already provides access to virtually the entire global music catalog for a comparable monthly fee. In effect, families are being asked to repurchase access to content they already pay for elsewhere, and not for additional exclusivity but for format and convenience. The value proposition therefore shifts from content access to hardware compatibility.

Ultimately, Merlin’s experiment highlights both the upside and the limits of diversification. The further the catalog moves from child-first use cases, the more it rests on the hardware alone to make the content feel newly appropriate for children. Not every adjacent format will carry the same willingness to pay or the same fit with the ecosystem.

Three strategic responses

Merlin’s experiment shows that breadth alone is not enough. Once a catalog is large enough to feel credible, the challenge becomes how to expand relevance without diluting the proposition or surrendering economics, coherence, and control. In practice, three responses stand out: original IP, platformization, and localization.

Owning the catalog: Original IP

The first response is to increase the share of content the platform actually owns. In kids’ audio, original IP is not just a creative nice-to-have, but a foundational strategic lever.

Virtually all companies in this space understand the stakes. Lunii has My Lunii Heroes, Yoto has Yoto Originals, and Eddi has developed its own original learning sets. Yet few seem to frame owned content as centrally, or pursue it as systematically, as tonies. In 2023, two of its top five franchises were proprietary. In 2024, the sleep-focused Sleepy Friends were the 4th best-performing IP in its global portfolio. And in Q1 2025, over 40% of its 68 new launches were “own content” Tonies.

The benefits are obvious. By owning their characters, story worlds, and the associated audio content, companies limit royalty exposure and improve their economics. More importantly, they gain total control over how a franchise is extended across products, formats, and geographies, without having to renegotiate rights at every step. This also makes it easier to build genuine exclusivity: if a proprietary character or format resonates, the value accrues to the ecosystem that created it instead of being redirected to a third-party.

That said, original IP is no panacea either. It bypasses royalties, but only to shift the burden onto the slower, and riskier, process of brand creation. Licensed hits borrow trust; original franchises have to earn it from scratch. The endgame is not to replace licensed IP altogether, but to use owned franchises to improve the mix over time — preserving the pull of major brands while building a more differentiated and ultimately more profitable content base underneath.

Opening the catalog: Platformization

Owning more content is only one way to scale the catalog. Another is to widen the supply base itself, while preserving the platform’s editorial and commercial boundaries. Producing high-quality content is slow, demanding, and hard to scale. Opening the system to outside creators expands the catalog without proportional in-house investment, while changing the device into a participatory medium.

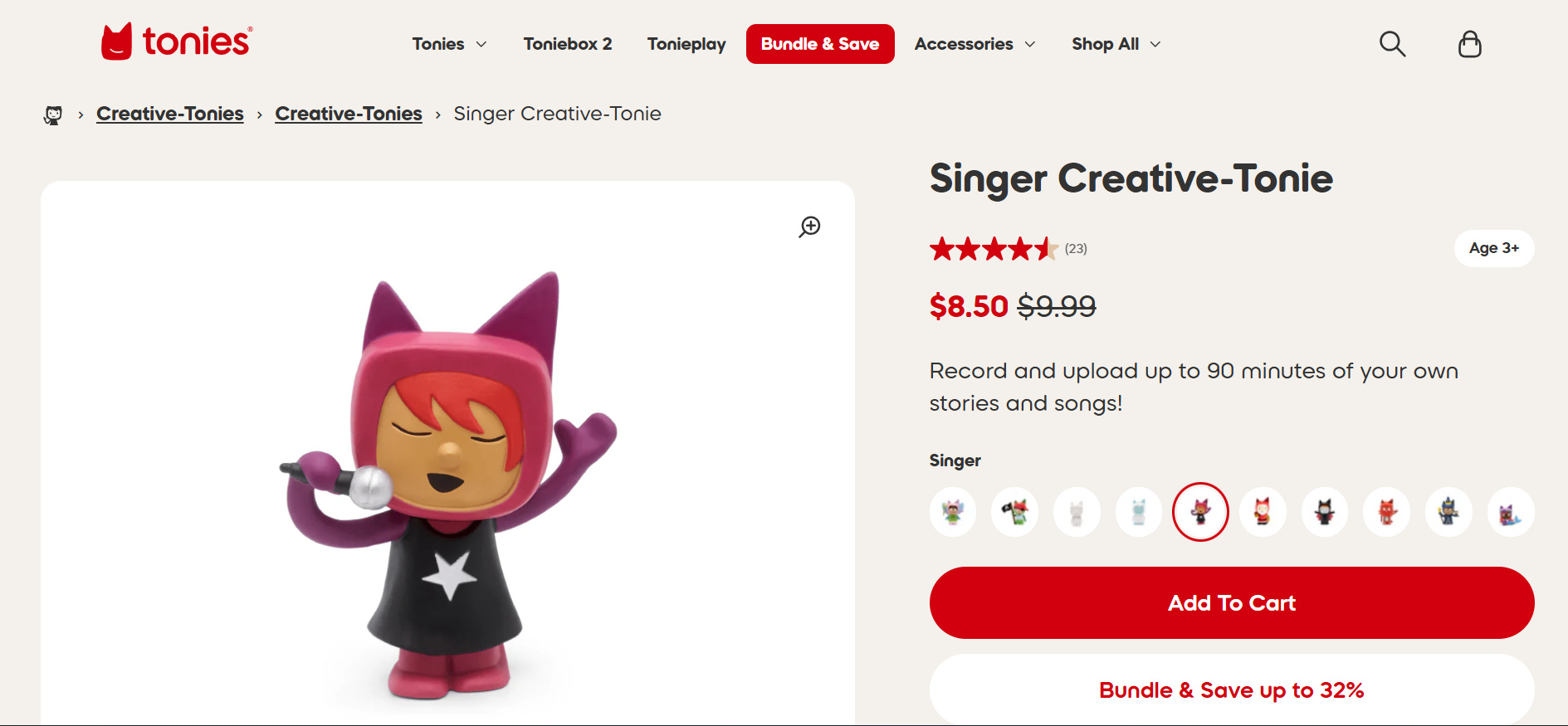

Not all players are approaching the opportunity in the same way. Most companies treat user-generated audio as a household-level personalization feature, where users can generate or upload content within tightly controlled boundaries. tonies’s Creative Tonies let users upload their own files and store up to 90 minutes of custom audio. Lunii and Joyeuse both offer their own version of a “studio”, where family members can record their own stories and songs to make them available from a kid’s speaker. These capabilities make the hardware part of a collective and transgenerational media ritual, rather than an individual one, reinforcing positive association.

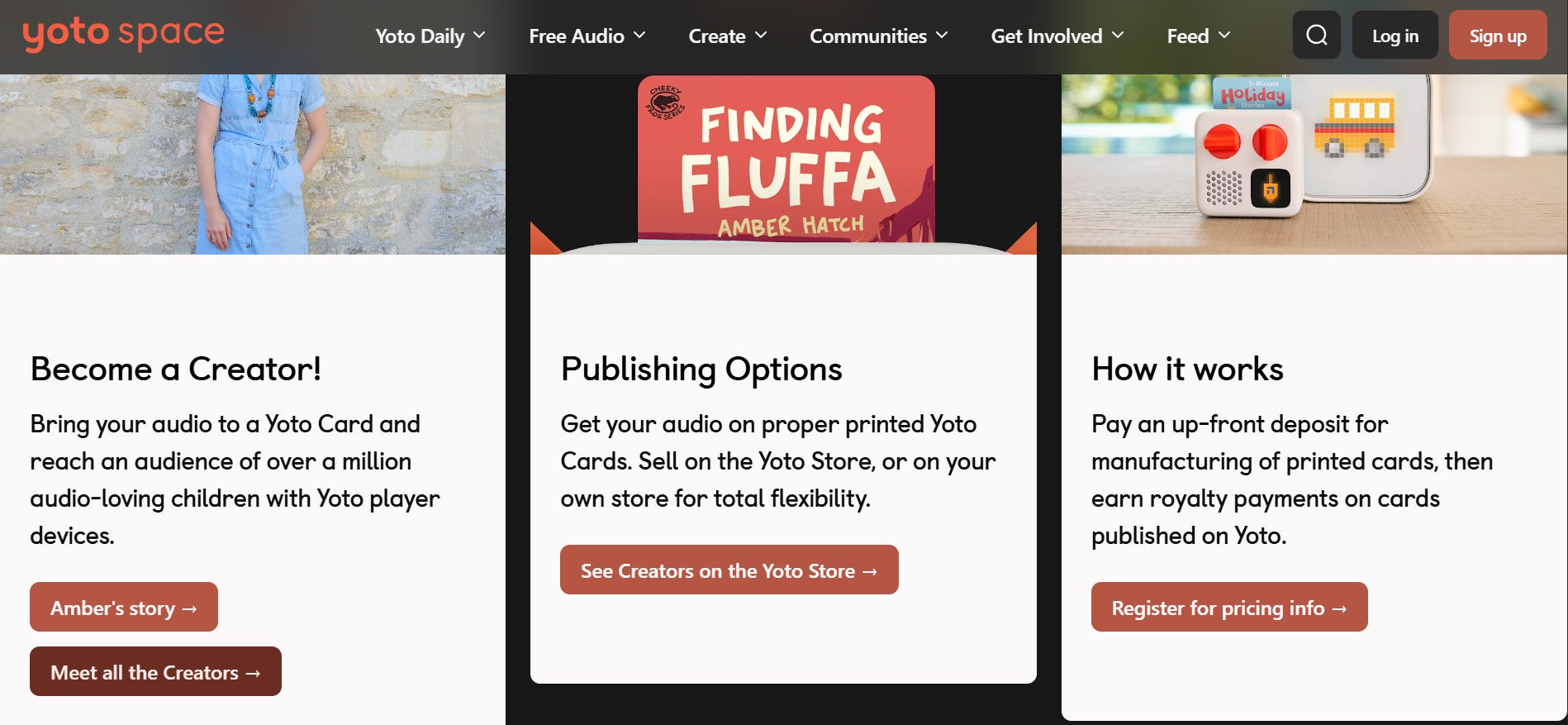

Yoto has pushed this logic the furthest. In addition to Make Your Own cards, which offer the expected family customization layer, it has built a more public-facing creator funnel. Through Open Mic, creators can publish free digital audio for the broader Yoto community, test concepts, and gather feedback. Through the Creators Program, some can then move into paid distribution via printed Yoto Cards sold either through Yoto’s own store or through their own channels “for total flexibility.” This amounts to a lightweight creator marketplace, with discovery, progression, and monetization built in.

The strategic leap, then, is from personalization to publication. In the first model, household-level customization may increase engagement, but it doesn’t fundamentally solve the catalog-scaling problem, since supply remains fragmented and private. Yoto is testing a different logic, one in which creator activity can start to benefit the wider ecosystem. What is created by one user is no longer just consumed by one family, but can feed catalog expansion, and eventually commerce, across the platform.

Still, platformization has clear limits in this category. The more public and open the model, the harder it becomes to preserve the editorial qualities and curation that underpinned these products. The risk is not just weaker content, but a catalog that feels less coherent and ultimately less trustworthy.

And those constraints do not apply only to proprietary content. For licensors like Disney or Hasbro, brand safety depends on context; too much openness could strain valuable business relationships. Maintaining control is therefore not just about safeguarding the user experience, but about preserving the partnerships that sustain the catalog and give it much of its appeal.

Extending the catalog: Localization

Increasing the supply is only one part of the scaling equation. The other is making the catalog travel — a challenge that becomes increasingly central as these companies expand internationally. This makes localization the third major lever, a driver of both growth and operational leverage, for structural reasons.

First, children need native-language content from day one: unlike adult video platforms, where subtitles or partial fluency can bridge gaps, kids’ audio relies on immediate comprehension. When sound is the whole product, there is no room for linguistic friction.

This matters all the more as these companies continue to scale internationally. Families in more than 100 countries have activated a Toniebox, and tonies’s growth is now increasingly concentrated outside its home market of Germany: in FY 2025, revenue rose 16% in DACH, versus 31% in North America and 64% in Rest of World. The further these businesses expand, the less growth can come from simply exporting a domestic catalog.

But localization does more than meet commercial necessity; it also strengthens these platforms’ educational case. As companies push further into learning, language stands out as an especially compelling category for parents who want playtime to feel productive. Foreign-language stories, songs, and vocabulary-based formats thus help their products align more closely with those aspirations.

The more global the IP pipeline becomes, the more localization turns from a cost center into a leverage point. The point of licensing Disney Princess or Peppa Pig is not to sell one market at a time but to use and amortize recognizable properties across as many territories as possible. Localization unlocks the full operational benefits of international licensing.

Capturing that potential is far from straightforward, however. International expansion still has to be rebuilt territory by territory, through local licensing negotiations, talent networks, and production workflows, and often cumbersome approval processes with rights holders. That capability can, in turn, become a competitive advantage in its own right. The better a company becomes at localizing major franchises across markets, the more attractive it becomes to IP owners looking for partners with genuine international reach.

On that note, it’s worth noting that the burden is not distributed equally across players. For tonies and Lunii, whose home markets are German- and French-speaking respectively, cross-border growth quickly implied linguistic adaptation. For UK-born Yoto, by contrast, English provided a much broader built-in runway across major markets, allowing the company to scale internationally before localization became equally urgent.

Yet despite this advantage, Yoto may well be the most forward-looking player in how it’s approaching the challenge. In July 2025, the company announced a partnership with AI voice scale-up ElevenLabs to let users switch supported cards into additional languages such as Polish, Romanian, German, Portuguese, and Hindi, “as simply as you can on Netflix.” If successful, this initiative would essentially decouple global catalog expansion from the slow, expensive, one-territory-at-a-time logic of traditional localization. Even with disclosure and quality checks, Yoto will need to tread carefully. Efficiency gains are only valuable if they do not erode the trust that made these ecosystems valuable in the first place.

At the end of the day, content is not just inventory in this category; it’s one of the main ways the business model either compounds or breaks. The objective is not to add IP, multiply formats, or broaden the catalog at any cost, but to build a content system that can grow while remaining economically sound and editorially coherent.

Product expansion

Once these companies have mastered storytelling and embedded themselves into family rituals like bedtime, the next logical move is to expand on that relationship. The opportunity here is to capture — and, of course, monetize — more moments of a child’s day.

No product exemplifies this dynamic better than Tonieplay. Introduced in 2025, it’s an interactive hardware add-on that brings audio-based gameplay to tonies’s core product, the Toniebox. As the audio unfolds, players respond to quizzes, make choices, and progress through the experience, turning what was previously just a listening device into a simple, tactile game interface.

Despite its novelty, Tonieplay closely follows tonies’s established playbook.

First, its promises are directly in line with tonies’s overall claims. Tonieplay Games, the company writes, “improve focus, enhance listening skills, and boost hand-eye coordination. Tonieplay’s engaging content helps kids develop problem-solving, decision-making, and critical thinking skills while supporting their self-confidence and empowering them to set and achieve goals.” In short, interactivity not only doubles down on the developmental benefits of listening, but extends them into more active forms of learning and cognitive engagement.

The model is familiar on the commercial side, too. Like the Tonies figurines, it opens up opportunities in both proprietary (e.g., Lalalinos, Time Academy) and licensed content (e.g., Gabby’s Dollhouse, Paw Patrol). In the latter category, tonies is already drawing from a diverse pool of properties, some of them coming not from film or television, but from the traditional board game industry. In Q3 2025, tonies extended its existing partnership with Hasbro — the owner of properties such as Peppa Pig, My Little Pony, and PJ Masks, all of which already have their own Tonies figurines — to the Tonieplay platform. In addition to Monopoly, two more of Hasbro’s board games are set to debut on Tonieplay “with new twists, concepts, and interactive moments.”

Where Tonieplay diverges more meaningfully from the rest of the tonies ecosystem is in the type of play it enables. While the Toniebox has embedded itself into family rituals, most of its core use cases remain inherently solitary. By contrast, Tonieplay Games allow for both solo and collective play from the same device. The format naturally lends itself to friendly competition or parent-child play, effectively turning the Toniebox into a screen-free alternative for family game time. In doing so, Tonieplay further expands the product’s role within the household, capturing moments of play that previously belonged to consoles or board games.

Educational offerings

The efforts kids’ audio companies have deployed to highlight their products’ educational merits were never aimed solely at parents. For the industry, schools and libraries represent a parallel, highly attractive channel, with not only scale and recurring budgets but also strong signaling power. Over the past few years, several players have made explicit moves in that direction.

tonies, for instance, has formalized its push through the “Tonies for Teachers” initiative. Though information is scarce, the company’s 2022 investor report suggested the program was active across multiple school districts and thousands of classrooms in the US, supported by teacher ambassadors. Meanwhile, Merlin recommends content adapted to different educational stages and lets teachers and administrators self-generate a quote directly from its website. It’s worth noting that the company already has a foot in the door through its co-owner Bayard, whose educational magazines are distributed at scale through long-standing school partnerships.

Realistically, these products are no substitute for teachers, nor are they adaptive learning platforms. Their appeal lies less in bold pedagogical promises than in their general benefits for kids’ attention and behavior. Today, companies like Merlin and Lunii cover nearly the full spectrum of everyday school needs: nursery rhymes for early learners, white noise and ambient music for rest time, audio documentaries and literary classics for older children... In practice, the device becomes less a teaching tool than a versatile classroom aid — tonies goes so far as to describe its Toniebox 2 as “an extra pair of hands in your classroom.”

There is, however, a clear tension: these devices were designed as a tactile, individual experience. The child is meant to operate the object on their own, with touch complementing sound. This aspect is largely lost in a classroom setting, where budget is constrained and kids are unlikely to have one device each. At home, these devices foster independence; in the classroom, they risk reverting to a more traditional, centralized listening experience.

Ultimately, the most compelling aspect of this educational expansion may not be institutional revenue per se, but rather the creation of a continuum of habit. Whether it be the morning listening circle at school or bedtime story at home, the same object, or at least the same interaction, anchors multiple moments throughout the child’s day and across multiple settings, reinforcing familiarity and attachment. Schools act less as a standalone revenue stream than as a high-trust funnel back into the consumer business.

Refurbishing

As installed bases grow, so does the flow of returned, replaced, and upgraded devices. The strategic question is whether that hardware becomes waste or productive inventory once more. At the same time, normal household churn is pushing more and more devices onto the secondary market, where brands can’t exert quality control and capture no share of the resale value. Together, these dynamics have pushed the industry to take action. What was once operational leakage is increasingly being captured and re-circulated in-house, turning refurbishing into a structured secondary channel with distinct but surprisingly compelling economics.

Companies are operationalizing this in distinct ways. Lunii sells officially reconditioned devices directly via its online store, clearly positioned as lower-priced entry points while maintaining in-house quality control. Tonies’ “Preloved Tonieboxes”, which are sourced from returns inventory and resold with a full two-year warranty, follow the same logic. Refurbished products unlock price-sensitive households without diluting the flagship line. Crucially, since content drives the bulk of lifetime margin, bringing more families into the hardware ecosystem, even at a discounted device price, enhances the overall economics of the platform.

Meanwhile, Yoto integrates refurbished units into its warranty process, reserving the right to replace faulty devices by sending a “refurbished one, tested and graded.” By reworking returned devices instead of scrapping them, it has turned support logistics into a circular loop rather than a cost sink, effectively improving gross margin over time.

The company also runs “Project Second Chance,” a donation program that repurposes returned or unused players via donations to local causes, a deliberate alternative to destruction while broadening access. While not a resale channel, strategic recirculation of that kind still indirectly supports the business. Not only does it reduce disposal costs, it also functions as a brand flywheel by improving visibility in schools without undercutting pricing in retail.

Where reconditioning becomes a real business opportunity is when it’s embedded into product lifecycle design. Lunii’s refurbished SKUs and Yoto’s warranty loops serve the same purpose: they keep hardware circulating within a controlled ecosystem. Lunii’s official exchange program goes one step further, letting customers return their old devices in exchange for a discount on the newer FLAM player, an attempt at managing upgrade behavior. In a category where hardware is the gateway to recurrent content sales, controlling and incentivizing circulation helps brands capture value across multiple usage cycles.

Experiential listening

As I’ve emphasized throughout this piece, kids’ audio is fundamentally a private medium. Its core value lies in solitary listening, family ritual, and everyday use inside the home. Even when the category reaches into more collective settings — most notably, schools — it’s still imagined through intimate use cases.

Precisely for that reason, public activations can do something ordinary advertising can’t: give otherwise private products greater cultural visibility and attach them to moments of play and togetherness.

tonies’ international go-to-market is a case in point. In the US, the company has backed family-facing events such as Los Angeles’s Great Big Family Play Day and built Toniepalooza, which blends live music, creative activities, and giveaways. Around the launch of Toniebox 2, tonies ran multiple activations across markets. In February, it marked the French release of two new Tonies figurines by throwing a kids-focused day party.

This has two main benefits. First, it helps brands move from mere product ownership to deeper brand affiliation. That’s especially valuable in a category where long-term economics depend not only on the initial hardware sale, but on repeat content purchases and ongoing engagement. As companies in the space invest more heavily in original IP, live events may become more central to franchise attachment and monetization. Top properties such as Miraculous Ladybug, PJ Masks, and PAW Patrol have already expanded into musicals with strong commercial results.

Second, activations give retailers and licensors visible proof of real-world traction. In the ecommerce era, a company that can generate buzz and attract families in-person looks more commercially credible. For retailers, that can justify more prominent placement. For licensors, it signals that a platform is not just a passive distribution channel but an active brand-building partner capable of amplifying demand around their characters.

Challenges

If the growth opportunity is real, so are the constraints. The more these companies expand beyond their original promise, the more sharply these pressures will be felt.

Competition

The easy phase of category creation is now long gone. In France, Lunii was once the undisputed category leader; then came Merlin, Tikino, tonies, and a growing cohort of challengers. Several of these players were able to break through with genuinely differentiated hardware and content propositions, reshuffling the competitive deck almost overnight. The impact is visible in Lunii’s own numbers. In December 2023, the company estimated it accounted for 63% of kids’ audio storyteller sales — a dominant share, but one that implicitly acknowledges erosion from what we can assume was a monopolistic position only a few years earlier. More tellingly, Lunii expected to sell 260,000 of its Fabulous Storytellers that year, down more than 25% from 350,000 the year prior, suggesting that category growth alone is no longer enough to offset competitive pressure.

Competition has only intensified since. Merlin has received sustained media attention and appears to be gaining commercial traction. Yoto, fresh off its 2024 funding round, has invested aggressively in brand awareness, running multiple campaigns in the Paris metro and positioning itself as a mainstream alternative rather than a niche import. Meanwhile, even though disclosures have been sparse lately, France also stands out as one of the most clearly localized markets in tonies’ communications, with country-exclusive Originals and ESG pilots.

The competitive landscape may soon shift again. Joyeuse was acquired by France’s Seico, its manufacturer, in 2023, then sold again to MGM Jouet in 2025. Bugali was placed under administration in October 2024, with a divestiture planu nveiled in February 2025. Whether this leads to consolidation, a brand relaunch under new ownership, or a quiet market exit remains to be seen. What is clear, however, is that the era of easy category creation is over; what comes now is a much tougher contest for attention, shelf space, and long-term household loyalty.

Supply chain disruption

Content may account for a growing share of value creation, but hardware and its underlying supply chains remain a critical constraint on the category’s economics. Narrower product portfolios increase dependence on a small number of components or manufacturing partners; when a crisis hits, that concentration sharply increases exposure.

Again, tonies’ investor disclosures offer a clear window into how these pressures have actually played out. In its 2021 annual report, management acknowledged being “confronted with shortages on key components like chips as well as higher prices for our raw materials.” What initially appeared as a temporary, COVID-era supply disruption would soon prove to be more structural. In 2022, the company described “significant and persistent macroeconomic challenges, characterized by drastic raw material price increases” and “tense supply chains.”

These headwinds were not prohibitive. By diversifying suppliers early, tonies even managed to improve its gross margin from 50.1 % in 2020 to 54.1 % in 2021, at a time when less operationally resilient players were scrambling for emergency sourcing. Supply chain robustness turned out to be a real competitive advantage.

Still, no matter how effectively they’re anticipated or absorbed, rising input and logistics costs add up. While temporary pricing adjustments can buy time, cost increases can only be passed on for so long before consumers start looking for cheaper alternatives. More importantly, even the most carefully designed supply chain only goes so far. Every major hardware refresh or new accessory reintroduces complexity, resetting parts of a company’s cost structure. Ultimately, supply chain resilience is not a permanent attribute but a capacity that is bound to be tested time and again.

Medium constraints

So far, an audio-first focus has served these companies well. By design, they’ve successfully framed audio not as a lesser substitute for screens, but as the superior medium, one that fosters concentration, imagination, and calm. That positioning has been central to their cultural legitimacy and commercial success.

But it also creates a structural constraint. Historically, the strongest children’s IP has usually scaled outward from visual formats. Starting from animation, Disney was able to branch into books, audio, toys, games, and theme parks. Today’s digital-native players like CoComelon operate on the same logic, establishing characters and aesthetics at scale on YouTube before naturally expanding into music, merch, and live entertainment.

Audio-first companies face the inverse problem. It’s not that they lack material. As I’ve explained, many have invested heavily in original IP, complete with characters and visual identities presented in apps and marketing assets. The issue is consistency. Having positioned themselves in explicit opposition to screens, they are largely locked out of experimentation with video. That effectively excludes them from the biggest and fastest-growing children’s medium and from the business that comes with it.

Moreover, video doesn’t just drive engagement; it imprints a character’s appearance and a world’s visual grammar in a child’s mind. Those cues lay a foundation that later sustains merchandising and long-term franchise value. By staying audio-only, these companies preserve coherence and trust, but at the cost of participating in the mostly visual economies that have historically turned children’s IP into global platforms. They can’t simply “add video” later without challenging the narrative on which their entire brands were built.

Aging out

However large their content catalogs may be, all kids’ audio hardware companies face the same structural challenge: their users will age out. As children grow, these devices stop competing mainly with books and toys and start competing with video — and increasingly, gaming too. The more constrained and single-purpose the product, the earlier this obsolescence is likely to kick in.

That leaves companies with two imperfect options. The first one, which I discussed earlier, is to broaden their content offering in order to follow users as their tastes mature. On that front, Merlin is arguably the best positioned. Backed by Radio France, the device gives access to a steadily expanding slate of podcasts aimed at older children and teenagers, including documentaries and even a weekly news format. It also integrates audio versions of Bayard magazines, extending the speaker’s relevance beyond pure storytelling and into everyday listening.

The second — more costly, but potentially more defensible — option is to transition users to a new device designed specifically for an older age group. This is the path taken by Lunii. After My Fabulous Storyteller (3–8), the company launched FLAM, an interactive audio player for ages 7–12 that introduces choice, progression, and reward mechanics inspired by choose-your-own-adventure books. Notably, the suggested age ranges overlap slightly, a smart way to smooth the handover from one device to the next rather than forcing a hard break.

It’s also telling that FLAM’s form factor edges closer to a handheld console or smartphone. Even in Lunii’s own marketing, children hold it the way they would a phone or a Game Boy. Coming from an audio-first company famously wary of screens, this feels like a quiet admission: to remain relevant as children grow, audio devices must increasingly borrow the ergonomics and interaction codes of the devices they’re competing with.

Kids’ audio hardware may still look like a niche, but it reveals a broader shift in what families now want from technology.

For decades, the dominant interfaces of childhood entertainment were visual: the television, the game console, the tablet, the smartphone. Each brought more content, more choice, and more stimulation. Even when parental controls exist, the underlying model remains centered around engagement: the goal is to keep the session going.

Kids’ speakers move in the opposite direction. Instead of screen abstraction, they strip the interface back to touch and sound. Their catalogs continue to expand, but the experience itself is finite. They support repetition without inducing fatigue. Today, that restraint is a strategic advantage. By making media accessible without making it bottomless, kids’ audio presents children with an environment parents can trust. At its best, it is not a lesser form of entertainment, but a different cognitive and emotional space.

That framing has profound consequences. If kids’ audio remains positioned only as a guilt-free substitute for video, it will stay defensive, its ceiling defined by what parents want to avoid. The better path is affirmative: audio as a medium of imagination, autonomy, and ritual.

Of all the challenges the category faces, aging out may be the clearest test of its ambition, because it comes with a built-in expiry date. The goal, then, should be to build a relationship strong enough that children can outgrow the hardware without leaving the medium behind.

Thank you for reading. If you’ve enjoyed this essay, please consider giving it a like and take a minute to share it with others. It really helps.

As always, I’d love to hear your thoughts! You can find me on Linkedin or on X, or just reply directly to this email.

Very cool article. Thanks for putting this in-depth analysis together. Loved it 🔥

This was such an in depth read! I've been curious about this for a while and it answered a lot of questions!